This Azad Engineering analysis examines one of India’s most advanced precision manufacturing companies, operating at the highest end of the global engineering value chain. With a ₹6,000+ crore order book, long-term contracts with global OEMs like GE Vernova and Siemens Energy, and industry-leading 36% EBITDA margins, Azad Engineering represents a structurally strong, non-cyclical manufacturing growth story.

Azad Engineering is emerging as one of India’s most strategically important precision engineering companies, operating at the highest end of the manufacturing value chain. With deep expertise in mission-critical rotating components, a ₹6,000+ crore locked-in order book, and long-term contracts with global OEMs such as GE Vernova, Siemens Energy, Mitsubishi Heavy Industries, Rolls-Royce, and Honeywell, the company represents a rare combination of engineering complexity, revenue visibility, and margin resilience.

Unlike traditional industrial manufacturers exposed to commodity cycles, Azad Engineering global precision manufacturing leader status is built on qualification-driven entry barriers, material science mastery, and multi-year OEM relationships that are extremely difficult to displace. This article provides a deep, investor-oriented analysis of Azad Engineering’s business model, competitive moat, financial performance, growth drivers, risks, and long-term outlook—going well beyond surface-level data.

Company Overview: Engineering at the Top of the Value Chain

Foundational DNA

- Founded in 1983, headquartered in Hyderabad

- Core focus: precision-forged and machined rotating parts

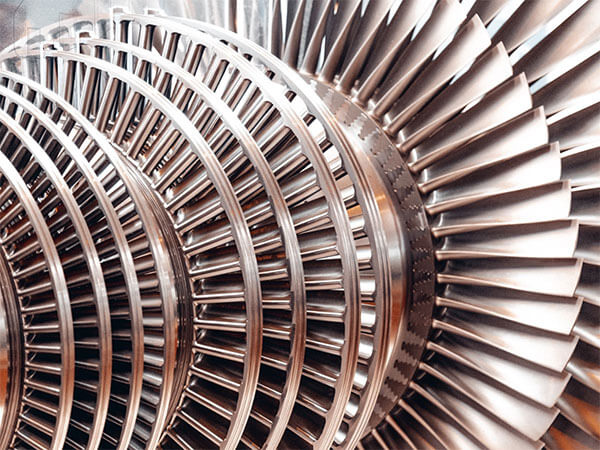

- Specialization in life-critical and mission-critical components

- Portfolio of 1,700+ qualified components

- Over 45 specialized manufacturing and metallurgical processes

- Proven track record of 3.9+ million zero-defect parts supplied

Azad Engineering does not operate in mass manufacturing. Instead, it sits at the intersection of metallurgy, aerodynamics, and precision machining, where failure is not an option. This positioning inherently limits competition and protects long-term profitability.

What Makes Azad Engineering Structurally Different?

1. Complexity-Driven Competitive Moat

Azad Engineering manufactures components that operate under:

- Extremely high temperatures

- Severe mechanical stress

- Tight aerodynamic tolerances

- Long operational life cycles

These include:

- 3D rotating and stationary airfoils

- Hot gas path components

- Compressor and turbine assemblies

OEMs cannot easily switch suppliers because:

- Qualification cycles take 3–7 years

- Certifications involve extensive testing, audits, and flight/engine trials

- Once approved, contracts typically run 5–10 years

This creates a structural lock-in effect, not a transactional relationship.

Material Science Expertise: The Real Entry Barrier

Azad Engineering’s true moat lies in its ability to consistently work with:

- Nickel-based superalloys

- Titanium alloys

- High-temperature steel variants

- Advanced forging + machining integration

These materials are essential for:

- Gas turbines

- Nuclear and thermal power plants

- Commercial and military aircraft engines

- Hydrogen-ready turbines

Very few Indian companies operate at this level of metallurgical sophistication, giving Azad Engineering a scarcity premium in global supply chains.

Global OEM Footprint: Blue-Chip Validation

Tier-1 OEM Relationships

Azad Engineering supplies directly to:

- GE Vernova

- Siemens Energy

- Mitsubishi Heavy Industries

- Rolls-Royce

- Honeywell

- Baker Hughes

These OEMs collectively control ~70% of the global gas turbine market.

Export-Led Business Model

- 92–94% of revenue from exports

- Customers spread across North America, Europe, and Asia

- India manufacturing base supports global energy and aerospace platforms

This global exposure not only diversifies revenue but also positions India as a strategic de-risked manufacturing hub for global OEMs.

Revenue Mix Analysis: Stability with Growth Optionality

Q1 FY26 Revenue Segmentation

- Energy & Oil & Gas: 81%

- Aerospace & Defence: 17%

- Others: 2%

The energy segment provides cash flow stability, while aerospace and defence act as a long-term growth lever.

Energy Vertical: Non-Cyclical by Design

Azad Engineering’s energy exposure is not commodity-linked but OEM lifecycle-linked.

Why This Matters

- Supplies critical turbine components, not discretionary parts

- Used across:

- Power generation

- Marine propulsion

- Combined heat and power (CHP)

- Hydrogen-enabled turbines

- Multi-year supply contracts smooth cyclical volatility

This makes earnings far more predictable than typical industrial companies.

Aerospace & Defence: The Next Growth Engine

While energy dominates today, aerospace and defence represent strategic upside.

Current Capabilities

- Compressor, combustion, and exhaust components

- Commercial jets and business aircraft

- Helicopters and defence aircraft

Safran MoU: A Strategic Signal

- Entry into defence engine programs

- Long qualification runway

- Potential for higher margins once scaled

Single-Crystal Blades: The Future Frontier

- One of the most complex aerospace components

- Very limited global supplier base

- Represents a step-change in technological capability

- Expansion planned over the medium term

Order Book Strength: Revenue Visibility at Rare Scale

Confirmed Order Book

- FY25 order book exceeds ₹6,000 crore

Key OEM Commitments

- Mitsubishi Heavy Industries: ₹1,387 Cr (5-year Phase 1 & 2)

- GE Vernova: USD 165.5 million

- Siemens Energy: USD 90.1 million

This order book provides multi-year revenue visibility, insulating the business from short-term macro uncertainty.

Financial Performance: Proof of Operating Leverage

Q2 FY26 Highlights

- Revenue: ₹143 Cr (+28% YoY)

- EBITDA: ₹51.4 Cr

- EBITDA Margin: 36.0%

- PAT: ₹33 Cr (+57% YoY)

- PAT Margin: 23.1%

H1 FY26 Performance

- Revenue: ₹277 Cr (+32% YoY)

- EBITDA Margin: 36.0% (vs 34.7% last year)

- PAT Growth: ~65% YoY

These numbers confirm that scale is improving profitability, not diluting it.

Why Margins Are Structurally Protected

Azad Engineering’s margins are supported by multiple layers of protection:

- High-value component mix (non-commodity)

- Domestic alloy sourcing approvals (Sunflag, Star Wire)

- ±5% raw material cost absorption band

- Natural FX hedge from export revenues

- Deep OEM trust reduces pricing pressure

Sustaining 36% EBITDA margins during expansion is rare in manufacturing and highlights business quality.

Capacity Expansion: Demand Is Not the Constraint

Current Manufacturing Footprint

- 4 facilities in Hyderabad

- ~20,000 sq. meters

- ~6 lakh machine hours

- 88.5% utilization

FY26–FY27 Expansion Plan

- ₹450 crore capex

- 3 new lean facilities for:

- Siemens Energy

- GE Vernova

- Mitsubishi Heavy Industries

- Backward integration into forging

Revenue Potential

- Incremental revenue unlock: ₹550 crore

- Medium-term revenue trajectory: ₹1,000 crore+

Execution: The Only Real Variable

Management has clearly articulated FY26 as a “stabilization year”, balancing:

- Parallel plant commissioning

- Workforce training

- OEM audits and qualification

- Working capital optimization

Despite this, guidance of 25–30% growth remains intact, indicating confidence in execution capability.

Key Risks Investors Should Track

No investment is risk-free. Key areas to monitor include:

- Execution risk across 8 new plants

- Aerospace qualification delays

- Working capital cycle improvements

- Dependency on a limited number of large OEMs

However, it is important to note that demand risk is minimal—execution discipline is the primary variable.

Industry Context: Precision Engineering Supercycle

Global trends favor companies like Azad Engineering:

- Energy transition requires efficient turbines

- Aerospace traffic growth drives engine demand

- OEMs are de-risking China-centric supply chains

- India emerging as a trusted manufacturing alternative

This creates a multi-year precision manufacturing supercycle, not a short-term boom.

Investment Thesis Summary

Why Azad Engineering Stands Out

- Operates at the highest complexity tier of manufacturing

- Locked-in relationships with global OEM leaders

- ₹6,000+ Cr order book ensures revenue visibility

- 36% EBITDA margins prove pricing power

- Capacity expansion supports long-term compounding

Who This Stock Is For

- Long-term investors

- Those seeking exposure to global manufacturing

- Investors comfortable with execution-led growth stories

Final Verdict

Azad Engineering global precision manufacturing leader is not a cyclical industrial story—it is a structural compounding opportunity built on trust, complexity, and global relevance. With demand firmly in place and execution as the key variable, the company is positioned to scale into a ₹1,000+ crore revenue platform while maintaining industry-leading margins.

Disclaimer

This article is for educational purposes only. It is not investment advice. Please consult a financial advisor before investing.

Disclaimer: This article is for educational purposes only and not financial advice. Investors should do their own due diligence before investing.

Disclaimer: The projections of potential returns are based on current market conditions and company performance. Actual results may vary due to various factors, including market dynamics, economic conditions, and changes in the competitive landscape. Investors should conduct their own research and consult with financial advisors before making investment decisions.

Multibagger Stocks breakout stocks

High-growth green investments

⚠️ Not SEBI Registered—just here to share insights | 🚫 No paid services—everything shared is entirely free! 🧠 Always Learning and excited to grow together in this journey of market exploration.

📲 Join Our Investor Communities

🔹 Join our Telegram Channel: Multibagger Hunts

🔹 Join our WhatsApp Channel: Click to Join

✅ Free access

✅ Instant alerts

✅ Curated research for serious investors

TwitterXWhatsAppThreadsTelegramFacebookLinkedInGmailEmailShare