Sakar Healthcare Business Model: From Exporter to Oncology Platform

Most investors track Sakar Healthcare only for oncology approvals and product pipeline growth. However, the real transformation lies in the Sakar Healthcare business model transition.

This is not merely a growth story. It is a structural shift from a volatile generic exporter to a semi-integrated oncology platform with improving margin visibility, recurring EU revenue, and backward integration leverage.

In this detailed analysis, we break down:

- Revenue engine transformation

- Margin expansion pathway

- Cash flow quality

- Re-rating triggers

- Execution risks

- Long-term investment thesis

This article is written to provide high-value, original insights for serious investors evaluating Sakar Healthcare.

Company Overview

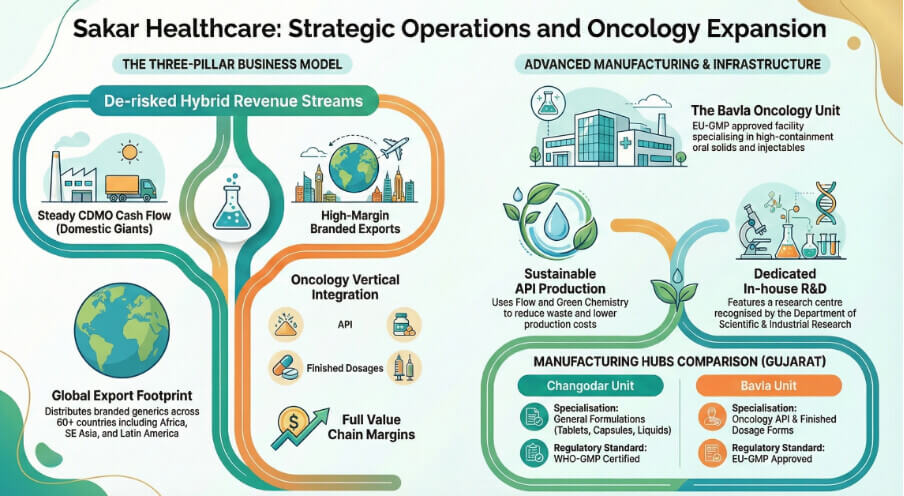

Sakar Healthcare Limited operates as an oncology-focused pharmaceutical manufacturer with a growing export footprint, particularly in Europe and regulated markets.

Key strengths include:

- EU GMP-approved oncology facility at Bavla

- Focus on high-value formulations

- Transition toward tech-transfer model

- Backward integration into APIs

The company is now entering a phase where business quality matters more than product approvals.

Evolution of the Sakar Healthcare Business Model

Old Model: Traditional Export-Led Growth

Earlier, Sakar operated largely as:

- Generic exporter

- Dossier-driven opportunity play

- Variable export margins

- High quarterly volatility

Revenue depended on:

- Spot export opportunities

- Domestic sales

- Opportunistic partnerships

This model often resulted in:

- Inconsistent EBITDA margins

- Working capital swings

- Earnings unpredictability

While growth existed, visibility was limited.

New Model: Integrated Oncology Platform

The new Sakar Healthcare business model rests on three structured growth engines:

- Oncology Formulations (FDF)

- Tech Transfer Model

- Backward Integration (API + CEP)

Let us examine each engine in detail.

1️⃣ Oncology Formulations – The Core Growth Driver

The finished dosage formulation (FDF) segment is now the backbone of scalable earnings.

Facility Strength

- EU GMP-approved oncology plant at Bavla

- Manufacturing capabilities:

- Oral solids

- Liquids

- Injectables

- Supplies to regulated and semi-regulated markets

Why Oncology Matters

Oncology formulations typically offer:

- Higher pricing power

- Lower commoditization risk

- Better margin profile

- Sticky partnerships

As export mix shifts toward EU-regulated oncology, revenue quality improves.

Strategic Implication

If EU commercialization becomes meaningful and recurring, this segment alone can transform valuation multiples.

2️⃣ Tech Transfer Model – Revenue Visibility Layer

This is where the business model shift becomes visible.

Instead of simply exporting generic products, Sakar now manufactures under partner marketing authorisations (such as global oncology players and established pharma distributors).

Typical Structure

- Forecast-based planning

- Minimum purchase commitments

- Trial shipment stage

- Batch-scale repeat orders

- Potential bi-monthly dispatch cycles

Why This Changes Everything

Traditional pharma exports are:

- Order-based

- Price-sensitive

- Highly volatile

Tech transfer introduces:

- Semi-contractual revenue visibility

- Repeat ordering rhythm

- Volume predictability

- Reduced quarterly volatility

This shifts perception from:

Exporter → Platform Supplier

That shift alone can justify re-rating.

3️⃣ Backward Integration – Margin Flywheel

Backward integration is the future margin lever.

Current Status

- 21 APIs developed

- CEP filings underway

- Gradual integration into EU supplies

Margin Impact

Without integration:

- EBITDA margin: ~25–26%

With integration:

- Margin pathway: ~30%

Strategic Advantage

Backward integration allows:

- Cost control

- Supply chain reliability

- Reduced raw material volatility

- Higher gross margins

If executed well, this becomes a structural competitive moat.

Revenue Mix Transformation

Old Revenue Mix

- Generic exports

- Domestic business

- Variable margin structure

Emerging Revenue Mix

- Oncology-dominant

- EU commercialization-led

- Tech-transfer driven

- API integrated

This is not incremental growth.

This is a quality upgrade.

Financial Quality Indicators to Track

To assess the Sakar Healthcare business model transition, investors must monitor the following:

Re-rating Triggers: What Will Actually Change Valuation?

Markets do not reward intent.

They reward execution proof.

Here are the real triggers.

1️⃣ EU Revenue Becomes Meaningful

Approvals alone do not matter.

Trigger indicators:

- EU revenue contribution visible in quarterly results

- Repeat dispatch cycles

- Growing regulated market mix

Once EU revenue becomes stable and predictable, earnings quality improves.

2️⃣ Tech Transfer Repeatability

Pipeline → Revenue → Repeat Orders

What to watch:

- Bi-monthly ordering rhythm

- Stable volume offtake

- Lower quarterly volatility

This signals platform stability.

3️⃣ Margin Durability Near 30%

Current EBITDA: ~26%

Management aspiration: ~30%

Re-rating requires:

- 2–3 consecutive quarters sustaining 28–30%

- Gross margin stability

- No sudden cost spikes

Margin stability = Multiple expansion.

4️⃣ Capex Completion & Operating Leverage

Major capex appears largely completed.

What this means:

- EBITDA should grow faster than revenue

- Depreciation stabilizes

- Interest cost plateaus

- PAT accelerates

If earnings scale without new capex burden, operating leverage becomes visible.

5️⃣ Cash Flow Tracking PAT

This is critical for valuation re-rating.

Ideal scenario:

- CFO ≈ PAT

- Working capital stable

- No large receivable build-up

When earnings convert to free cash flow, execution discount disappears.

Margin Structure Deep Dive

| Scenario | EBITDA Margin | Key Driver |

|---|---|---|

| No Integration | 25–26% | External API sourcing |

| Partial Integration | 27–28% | Blended cost advantage |

| Full Integration | 29–30% | Internal API + EU mix |

Sustained 30% margin would reposition Sakar among high-quality oncology players.

Industry Context: Why Oncology Is Attractive

Globally, oncology remains one of the fastest growing therapeutic segments.

Key industry tailwinds:

- Aging population

- Increasing cancer incidence

- Higher treatment penetration

- Regulatory acceptance of generics

India’s oncology manufacturing ecosystem continues to grow, supported by:

- Cost advantage

- Regulatory expertise

- Skilled talent pool

Understanding sector trends helps contextualize Sakar’s positioning.

Risks Investors Must Track

No transformation story is risk-free.

Execution Risk

- EU commercialization delays

- CEP approval delays

Working Capital Risk

- Receivable stretch

- Inventory build-up

Pricing Risk

- EU price erosion

- Tender-based compression

Regulatory Risk

- EU inspection observations

Execution consistency will determine whether the re-rating materializes.

Valuation Framework: What Changes the Multiple?

Currently, exporter-type pharma companies trade at lower multiples due to volatility.

If Sakar demonstrates:

- Revenue visibility

- Margin durability

- Cash flow conversion

- Lower earnings volatility

It may transition to:

Growth exporter multiple → Platform oncology multiple

That shift can be powerful.

Long-Term Investment Thesis

The Sakar Healthcare business model transition suggests:

- Improving revenue quality

- Rising export contribution

- Structural margin expansion

- Free cash flow potential

However, the story must be validated by numbers, not commentary.

What Makes This a Quality Upgrade Story?

This is not about:

- Dossier count

- Approval announcements

- Management guidance

It is about:

- Revenue mix shift

- Visibility improvement

- Margin structure durability

- Cash conversion

Markets re-rate stability.

If Sakar proves repeatability, volatility discount reduces.

Key Monitoring Checklist for Investors

Every quarter, track:

- EU revenue % contribution

- EBITDA margin trend

- API integration progress

- Receivable days

- Operating cash flow

- Capex intensity

Create a quarterly tracking sheet to measure execution.

Final Thoughts: Is the Re-rating Sustainable?

The Sakar Healthcare business model is evolving into a more integrated, oncology-focused platform.

But the market will demand:

- 3–4 quarters of proof

- Stable margins near 30%

- Visible EU repeat orders

- Cash flow consistency

If delivered, valuation expansion becomes logical.

If execution falters, stock may remain range-bound.

The opportunity lies in identifying the inflection point early.

⚠️ Disclaimer

This content is for educational purposes only and not financial advice. Please do your own research before investing.

Disclaimer

This article is for educational purposes only. It is not investment advice. Please consult a financial advisor before investing.

Disclaimer: This article is for educational purposes only and not financial advice. Investors should do their own due diligence before investing.

Disclaimer: The projections of potential returns are based on current market conditions and company performance. Actual results may vary due to various factors, including market dynamics, economic conditions, and changes in the competitive landscape. Investors should conduct their own research and consult with financial advisors before making investment decisions.

Multibagger Stocks breakout stocks

High-growth green investments

Solar Technology Analysis

⚠️ Not SEBI Registered—just here to share insights | 🚫 No paid services—everything shared is entirely free! 🧠 Always Learning and excited to grow together in this journey of market exploration.

📲 Join Our Investor Communities

🔹 Join our Telegram Channel: Multibagger Hunts

🔹 Join our WhatsApp Channel: Click to Join

✅ Free access

✅ Instant alerts

✅ Curated research for serious investors

TwitterXWhatsAppThreadsTelegramFacebookLinkedInGmailEmailShare